On Easter morning people speak of resurrection. I speak of capitalism. The metaphor is not accidental — the system we are accustomed to periodically declaring dead repeats the same movement with astonishing patience: it falls, it breaks, and it returns. Different, but it returns.

This text is about mechanics. About a structure identified a hundred years ago by a Russian economist who studied in St. Petersburg and was shot in Moscow for identifying it. About a rhythm that determines why financial crises come in waves, why technological revolutions have their own time, and why the current decade — regardless of how politically chaotic it is — can be structurally understood.

But here is what won’t let me go: four completely different researchers — Kondratiev, Benner, Dalio and Šmihula — working with different methodologies, in different eras, different cultures, arrived at strikingly similar conclusions about the rhythm of capitalist cycles. That convergence is not a coincidence. It is a pattern worth taking seriously.

The Man Who Counted Fifty-Year Cycles

Nikolai Kondratiev was born in 1892 in a village a few hundred kilometres from Moscow, which at the time was one of those Russian provinces where life was very concrete, very hard and very far from Petersburg. A family of Komi origin, farmers. He studied economics in Petersburg, became acquainted with the cooperative movement and peasant economic theory, and in 1917, at 25, found himself in the place where many young, talented people found themselves in the revolutionary era: trying to find his footing in a shifting reality.

In the structure of Kerensky’s Provisional Government he held the post of Deputy Minister of Food Supplies. For five days. In October the Bolsheviks came.

Kondratiev did not emigrate, as many intellectuals in his circle did. He stayed. Not because he believed in communism — but because he believed in numbers. Numbers don’t care what system is in power. In the 1920s in Moscow he founded the Conjuncture Institute — one of the most serious economic analysis centres of its time in the world. He collected price series, production data, trade volumes across the major capitalist economies — Britain, France, Germany, the United States — going back to the late 18th century. He was looking for patterns.

He found one. Long waves of 45–60 years in economic activity. Periods of growth, followed by periods of stagnation and crisis. The structure was recognisable across different countries and different time periods. He published this in 1925.

He tried to dress the theory in Marxist terminology — calling capital investment cycles “systemic contradictions,” crisis a “dialectical necessity.” An intellectual game with ideological censorship that he won technically, but lost strategically. The essence remained the same: capitalism cyclically regenerates. Such a conclusion was always unacceptable.

Soviet power tolerated a certain intellectual diversity during the New Economic Policy era — a hybrid system that allowed some private economic activity alongside the state sector. In 1928 the NEP was closed. Centralised planning. Stalin’s system demanded not analysis, but confirmation.

Kondratiev’s theory became politically intolerable. Simply because it was good, but with an unacceptable conclusion: capitalism would not collapse in history, it simply goes through cycles, through winters, and emerges from them. Confirmation of capitalist resilience — in Stalin’s era — was tantamount to sabotage.

He had enough authority that his findings could have had influence.

In the 1930s he was arrested. Accused of peasant nationalism and terrorism. Five years of interrogations, transfers, prisons. On 17 September 1938 he was shot at the Kommunarka shooting range near Moscow. He was 46.

Letters survive from the prison period. He wrote to his wife Yevgenia and daughter Elena — she was born around 1919, and when her father was arrested she was about ten years old. The economist who counted fifty-year cycles wrote letters from prison to a daughter growing up without him.

The moment you understand that — that a man who counted half-century rhythms was writing letters to a daughter who never saw him growing up — something happens to the abstract theory. It becomes concrete. He didn’t know if anyone would read those numbers. But he counted them.

What Nikolai Actually Said

Kondratiev’s core idea looks simple on the surface: the economy has long cycles lasting roughly 45–60 years. More deeply — it is a complex theory about how capital accumulates, depreciates and renews. The cycle’s upswing begins at an infrastructural moment: a new technology reaches the point where it can be deployed at mass scale. The steam engine, railways, electricity, the automobile, the internet — each time there is a moment when technology transitions from experiment to infrastructure. This requires enormous investment, investment requires credit. Credit expands. New jobs, new sectors, optimism. Spring and summer.

But infrastructure cannot grow forever. It matures. Returns on new investment diminish — because the best sites are already built, the best deployment already used. Credit shifts from a financing instrument to a speculative one. The system moves from growth to redistribution — who captures the gains of the existing infrastructure. This is autumn. Then winter — crisis, deflation or inflation, collapse of overextended structures, painful rebalancing. And then — a new technological base, new capital, new spring.

The term “creative destruction” — Schumpeter applied it here. The crisis destroys the old to make room for the new to take its place in new areas. The term is beautiful, but for people whose jobs are in what is being destroyed, there isn’t much beauty here.

A schema that explains everything explains nothing specifically. But when it explains almost everything — then it is worth listening.

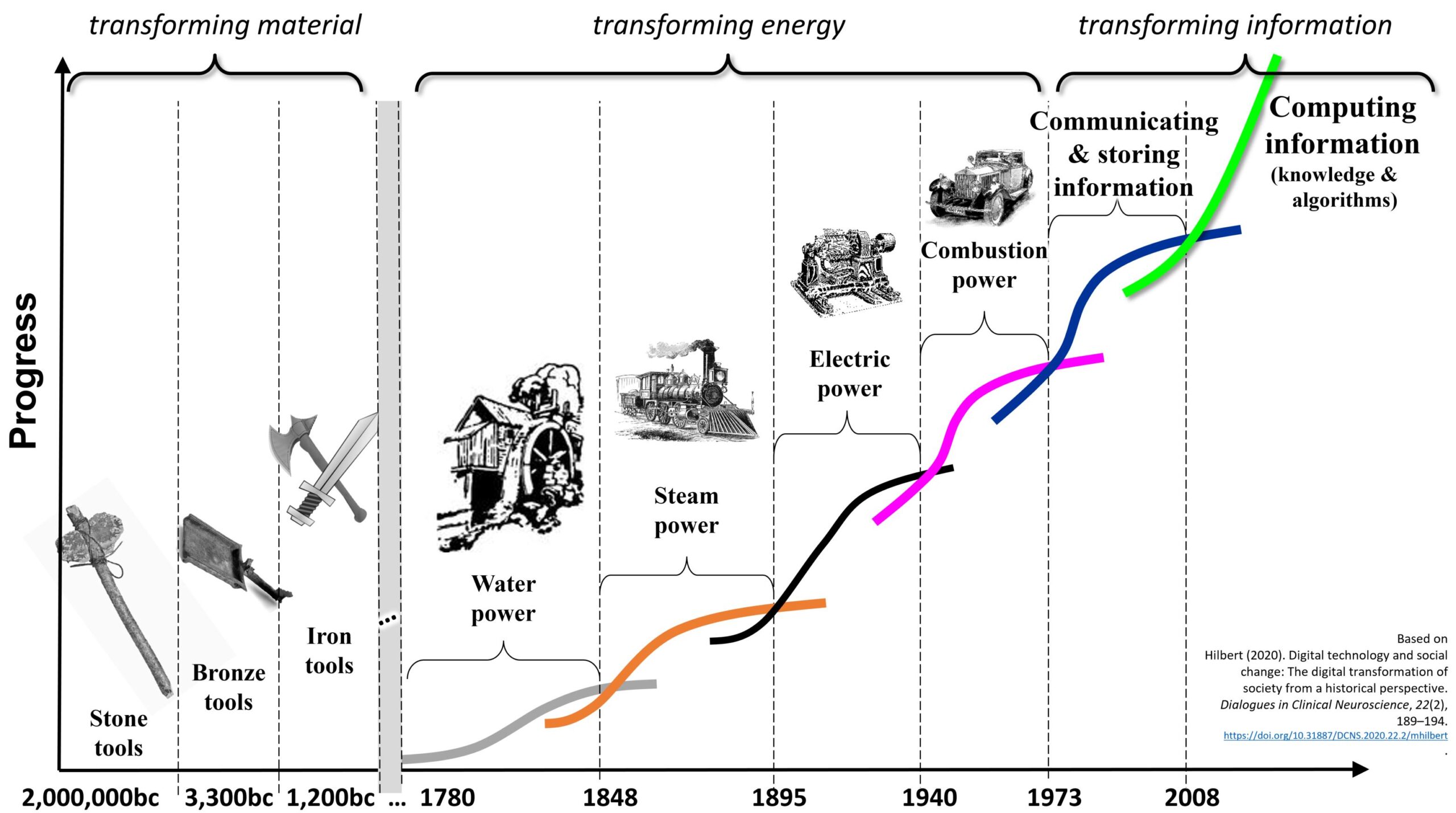

Five Waves: From Steam to the Internet

Researchers have identified five historical K-waves. In each — the technological engine and financial structure are inseparable.

The first wave, roughly 1780–1842. The steam engine and textiles. The first industrial revolution in England — not just a technological breakthrough, but a capital revolution. For the first time in history it became possible to systematically repeat production at scale. Mechanised textile factories. Canal infrastructure. The financial innovation was the joint-stock company — a mechanism for aggregating capital beyond individual family wealth. The wave’s winter — crisis of the early 1840s.

The second wave, roughly 1842–1897. Railways and steel. This was the wave that created global capital markets. The railway required capital at a scale no single state or family could provide. Bond markets — the mechanism for financing infrastructure through distributed capital. The railway network connected markets, reduced the cost of transporting goods, created the logistics infrastructure that made mass markets possible. The wave’s peak — around 1873, followed by the Long Depression.

The third wave, roughly 1897–1940. Electricity, automobiles, chemistry, the telephone. This wave changed the texture of everyday life more deeply than any previous one — not just production, but how people live, move and communicate. The peak — 1929. The Great Depression was not an accident or the greed of bank executives — it was the winter of the third wave, the collapse of the credit structure that had financed the electricity and automobile boom. Systemic, structural.

The fourth wave, roughly 1940–1980. Oil, petrochemicals, mass production, the welfare state. All dollar strength lay in oil. The US after World War II shaped the Bretton Woods order — the dollar became the world’s reserve currency, pegged to gold, and the petrodollar system locked in this hegemonic architecture. The welfare state — social insurance, pension systems, healthcare — arose not from generosity, but from a political response to the crises of the previous wave. Peak — the oil shocks of the 1970s.

The fifth wave, roughly 1980 to today. Information technology, the internet, globalisation. This wave created value in ways previous waves had not: not from physical assets, but from networks, platforms, data. The dot-com boom was the speculative excess of the wave’s autumn. The 2008 crisis — the winter of the credit structure that had accumulated over the wave’s growth. We are now in the wave’s late phase — deep winter or early spring, depending on how you read the signals.

In each of these waves — one observable principle: the peak always coincides with credit detaching from the real economy. In the growth phase credit finances real investment. In the maturity phase — speculation. Financial capital always seeks the best return, and when real projects mature, capital naturally shifts to the asset price game. You cannot blame market participants — they are acting rationally. But collectively rational behaviour creates systemic instability.

The first time I saw this diagram a few years ago I immediately felt that anxiety a person feels when they find the point on the map where they are standing. Not comfortable knowledge. Structural knowledge.

Four Seasons

Kondratiev himself did not use the four-seasons metaphor — that was added by later interpreters, most notably by analysts in the US in the 1990s and 2000s. But the metaphor captures the structure well.

Spring — recovery. New technological infrastructure begins to generate real productivity. Credit expands on a healthy foundation. Employment grows. Optimism returns, but moderately — the previous winter’s scars are still fresh.

Summer — growth with signs of overheating: inflation, social conflicts over how the fruits of growth are distributed, sometimes geopolitical tension. Summer always ends with a shock.

Autumn — the most dangerous phase, because it looks the best. Credit expansion detaches from the real economy. Asset prices rise not because the asset generates more income, but because everyone expects it to keep rising. Borrowing becomes the norm. Financial euphoria as the season’s defining feature. Newspapers write that “this time it’s different.”

Winter — crisis. The system ejects what has grown old. Asset bubbles burst. Debt deflates, or — when the state doesn’t want to allow deflation — is monetised: the central bank expands the money supply, inflation becomes an indirect mechanism for writing off debts. Bankruptcies, unemployment, political instability. And simultaneously — structural necessity: capital trapped in old structures is forced to move to new areas. Winter is painful. Winter is also necessary.

The Benner Cycle

Samuel Benner was an Ohio farmer — not an economist, not an academic. The Panic of 1873 led him to bankruptcy. Calculating pig iron prices, hog and corn price swings over decades, he published in Cincinnati in 1875 a small book with forecasts. His model — three alternating market rhythms: an 8–9–10 year peak sequence, an 11–9–7 year trough sequence, and a 16–18–20 year panic rhythm. Strikingly accurately, this model fitted the 20th century market shocks that occurred after Benner’s death. I wrote about this in more detail in the Benner cycle analysis, but briefly: according to Benner’s model panic rhythm, the 2025–2026 period falls into a difficult point, followed by a recovery phase. This aligns with the K-wave winter logic.

Benner did not explain why cycles repeat. He simply observed that they did. That is the most honest scientific position: I see a pattern, I don’t fully understand why it exists, but I’m recording it.

Ray Dalio and the Big Debt Cycle

Ray Dalio — founder of Bridgewater Associates, one of the world’s largest hedge funds. His framework is different from Kondratiev’s, but arrives at structurally similar conclusions. Dalio identifies a “long-term debt cycle” of roughly 75–100 years — a period during which debt accumulates to a level where the system can no longer tolerate it, and a painful reset occurs.

The mechanism is simple. Debt enables more spending than income allows. This stimulates growth. But debt has a ceiling — when interest payments become the most important line in the budget. More simply: one day interest payments become the most important budget line item — and from that moment on the finance minister has no real freedom of manoeuvre. US public debt today, as a percentage of GDP, is higher than at any point since the end of World War II. Interest payments are approaching the size of the defence budget. The system is not sustainable. Dalio’s long cycle winter and the K-wave winter coincide in this period.

Zeeberg’s Market Analysis

Henrik Zeeberg is a Swedish market analyst. His work revealed a visual parallelism between the 2020–2026 Nasdaq dynamics and the structure of the 1920s bubble — not a general similarity, but a very specific sequence of price movements with recognisable phase patterns. This is not directly K-wave theory. But it is a visual reflection of the euphoria profile typical of autumn: market behaviour that structurally resembles the last breath before winter. What interests me: not whether Zeeberg’s parallel plays out exactly, but that a researcher working from a completely different starting point arrives at the same temporal zone. 2025–2026 as a structural inflection point.

Šmihula’s Technological Waves

Daniel Šmihula — a Slovak political scientist — proposed a modification of Kondratiev’s theory in 2009. His observation: waves are getting shorter. The first industrial wave lasted about 60 years. The next — shorter. Each subsequent technological revolution compressed more quickly, because in a globally connected world technologies spread and are adopted faster. His sixth wave — the artificial intelligence wave — by his model should begin around 2020 and last until roughly 2040.

Four completely different researchers — different methodologies, four different data sources, and all indicators pointing to the same period: 2020–2035 as a decade of structural transition.

There is also a fifth aspect that makes this synthesis particularly important — the intersection with the hegemonic cycle. Ray Dalio and other cycle analysts observe that K-wave winters historically often coincide with hegemon shifts: the old global power weakens, a new one rises, a structural conflict occurs between them. British hegemony was replaced by US hegemony precisely as the fourth K-wave transitioned from winter to spring. Today US hegemony is being pressured by China — and this geopolitical redistribution is happening at the same time that the K-wave, Benner’s panic rhythm and Dalio’s long debt cycle all point to a structural crisis. The hegemonic cycle transition and K-wave winter moving together create a stronger transformation thesis than either individually.

This isn’t a prophecy. It is a structural context for reading the current moment.

Where Are We?

I have a family, savings and at least a little responsibility for the next decade. The question “winter or already spring” is not abstract — it changes how you think about professional direction, about assets, about where you are vulnerable.

The winter signs are clear. The global debt structure — the combined debt of states, corporations and households — has reached historic highs. Central banks in 2022–2023 raised interest rates faster than at any period since the 1980s — a structural signal that the system could no longer tolerate the credit price levels that existed during the fifth wave’s autumn. Real estate markets in several countries began to correct — not catastrophically, but the correction is happening. SVB and Credit Suisse were the first large winter casualties — smaller than in 2008, but structurally similar: institutions that existed and grew in an ultra-low-interest environment, killed when that environment ended. The geopolitical redistribution — the US-China rivalry structurally resembling the British-American transition of the early 20th century — is also a K-wave winter marker.

But the essential question that troubles me. Spring by K-wave logic does not begin when markets rise from new technology euphoria. It begins when new technological infrastructure starts generating real, measurable productivity in the broad economy. The internet wave really began to change the economy not in 1999, when there was dot-com euphoria, but in 2005–2012, when broadband internet, Google, Amazon and mobile devices became real infrastructure, changing how business is organised, how warehouses are managed, how information is searched. AI today is closer to 1999 than to 2008. Euphoria first, infrastructure — later.

This means one possible scenario: a short-term AI correction — winter’s last chord — before the true spring, which will begin in 2028–2032, when AI infrastructure is sufficiently widespread to generate macroeconomically significant productivity growth. If that’s the case, then right now we are in the most uncertain zone: winter’s end, but not yet spring’s beginning. The worst for short-term speculation, the best for long-term positioning.

What to Watch

If this analysis has value, concrete signs over the coming years will either confirm or refute it.

The first: the share of US debt interest in the federal budget. When it exceeds defence spending — and it is approaching that rapidly — this will be a structural moment showing the depth of Dalio’s cycle. At that moment any US administration will face a concrete choice: cut other spending (politically difficult), or monetise the debt — expanding the Fed’s balance sheet and inflating, which is effectively a tax on savings. This choice will show which path the political response to winter takes: reconstruction or destruction.

The second: AI productivity data. If in 2–3 years artificial intelligence fails to generate measurable macroeconomic productivity growth — not just anecdotal cases, not just corporate narratives, but real data on GDP growth, labour market change or return on investment — the sixth wave thesis will need revision. Either the wave is real but delayed, or it was overestimated.

The third: geopolitical signals. If the US-China rivalry moves from trade-economic to direct military — K-wave winter historically is when hegemonic transitions turn violent. That would not be the first time. The British-American transition was relatively peaceful. The German challenge of the early 20th century was not.

The Sceptic’s Voice

I must be honest about the critique, because this analysis deserves it.

The first: K-wave theory is not falsifiable in the strict scientific sense. If a crisis happens — it confirms the theory. If it doesn’t — you can always say the wave shifted, or was delayed, or was absorbed by policy. A theory that can explain anything doesn’t specifically explain anything. That is a serious critique, not a trivial one.

The second: different economists give different K-wave dates. There is no consensus even on which wave is which, when it started or ended. When a theory is this flexible on dates, you need to honestly ask about its rigour. A theory that can explain anything in fact explains nothing specifically.

The third: AI as the sixth wave engine may turn out to be overvalued. Technology waves generate real economic growth only when they create mass-use infrastructure — a process that historically took 10–20 years after the first browser or first commercially used computer. AI may generate productivity, but may also have a similar delay. And a delay means the true spring is still far off.

The fourth, which troubles me most: when Benner, Dalio, Zeeberg and Šmihula all point to the same period — that is not independent confirmation. These researchers know each other’s work, or share common intellectual sources. The apparent convergence may be an artefact of shared intellectual tradition, not independent empirical discovery. True independence would require researchers who had never encountered each other’s frameworks arriving at the same conclusions from raw data. That is rare.

Capitalism as Phoenix

Every K-wave transition has cost something. Usually most to those near the disappearing sectors. In the 1840s those were textile artisans in England. In the 1930s — farmers and industrial workers. Now — some services and knowledge work. I won’t speak here of serenity about that. Only of clarity: this is not an anomaly. This is the cycle. And knowing where you are in the cycle doesn’t protect you from its costs — but at least lets you make decisions with open eyes.

In the 1830s agricultural England gave way to industrial. Not smoothly — there was the Luddite rebellion in England, people smashing machines because their jobs were being eliminated. They didn’t stop the machines. But their pain was real, and to dismiss it as “the price of progress” is to speak from a very comfortable position.

In the 1930s the collapse of old financial structures gave birth to the Bretton Woods system, the social state, the mass consumption society. Those decisions were made from experience that a free market without stabilisers can produce political catastrophes. Weimar inflation, the Great Depression, Hitler’s rise to power — these were winter consequences when the political response was destruction, not reconstruction. In 1945–1980 a different direction was chosen.

In the 1970s the industrial welfare state gave way to financial capitalism and globalisation. That too was a choice — not a mechanical consequence of the K-wave. Choices made in winter determine the shape of the next spring. The phoenix always returns. It’s just that not those who remained standing at the doors of a disappearing sector ride it.

Sources

1. Kondratiev, N. D. (1925). “Bol’shie tsikly kon”yunktury” [The Long Cycles of Conjuncture]. Voprosy Kon”yunktury, 1(1), 28–79. [English translation: Kondratiev, N. D. (1984). The Long Wave Cycle. Richardson & Snyder.]

2. Schumpeter, J. A. (1939). Business Cycles: A Theoretical, Historical, and Statistical Analysis of the Capitalist Process (2 vols). McGraw-Hill. [The naming of Kondratiev waves and the three-cycle system.]

3. Šmihula, D. (2009). “The Waves of the Technological Innovations of the Modern Age and the Present Crisis as the End of the Wave of the Informational Technological Revolution.” Studia Politica Slovaca, 1, 32–47.

4. Šmihula, D. (2011). “Long Waves of Technological Innovations.” Studia Politica Slovaca, 2, 50–67.

5. Dalio, R. (2021). Principles for Dealing with the Changing World Order: Why Nations Succeed and Fail. Simon & Schuster.

6. Benner, S. T. (1875). Benner’s Prophecies of Future Ups and Downs in Prices: What Years to Make Money on Pig-Iron, Hogs, Corn, and Provisions. Robert Clarke & Co., Cincinnati.

7. Perez, C. (2002). Technological Revolutions and Financial Capital: The Dynamics of Bubbles and Golden Ages. Edward Elgar.

8. Grinin, L., Devezas, T. C., & Korotayev, A. (Eds.) (2012). Kondratieff Waves: Dimensions and Prospects at the Dawn of the 21st Century. Uchitel Publishing House.

9. Korotayev, A. V., & Tsirel, S. V. (2010). “A Spectral Analysis of World GDP Dynamics: Kondratieff Waves, Kuznets Swings, Juglar and Kitchin Cycles in Global Economic Development, and the 2008–2009 Economic Crisis.” Structure and Dynamics, 4(1).

If this text helped you see the context that’s missing from daily news — share it with someone who cares about it too. The best conversations begin with a good question.