Tactics Sold as Strategies

In 2007 I was twenty-three. I took out a loan, bought an apartment – and six months later I was counting cents at the grocery store. I believed what everyone believed: a long horizon smooths everything out. It did – but only after six years. And those six years I paid for a mistake I made not because I invested, but because I didn’t understand where I stood in the cycle.

This letter is about that mistake. And about why millions of people repeat it every month, on the fifteenth, automatically transferring a hundred euros into a fund that was sold to them as a “strategy.”

This mistake is not accidental. It is systematically manufactured. Over the past forty years the financial industry has built infrastructure – funds, platforms, automated transfers, pension savings schemes – designed to make regular investing feel like a strategy. It is not a strategy. It is a tactic. And the difference between those two things is the difference between understanding the cycle and simply hoping for the best.

Regular investing is better than not investing at all. Schwab, Vanguard, Morningstar – all have research confirming this. For the average person who cannot tell a bubble from a bottom, DCA is the best advice.

But “best advice for the average person” does not mean “best advice.” It means: we don’t believe you’ll be able to understand the cycle, so just buy every month and don’t ask questions.

DCA is a financial industry product. Easy to sell, easy to explain, generates stable fees for the manager. The fund takes its half percent or full percent – regardless of whether the market is rising or falling. Everything is fine for them. And for you?

Understand the mechanism. The fund manager’s income is a percentage of assets under management – not of returns. It doesn’t matter to them whether your portfolio grew or stood still over five years. What matters to them is that the total assets under management keep growing – and they grow every month when you transfer. This is called the “assets under management” model, and it is brilliantly constructed: the risk is yours, the reward is theirs. When the market rises, they earn more. When it falls – they earn less, but they still earn. And in bad times there’s no one to blame – not the strategy, not the person, not the decision. Just “the market.”

Simple Math

The market is at 100. Over the next year it drops to 60 and then over a couple of years climbs back to 120. Three people, three strategies.

The DCA person bought a little every month throughout the whole period. Average price – roughly 85–90. When the market reaches 120, their return is around 30–40 percent.

The person who understood the cycle: sat on cash while everyone was buying at 100. Bought at 60–65 while everyone was selling. When the market reaches 120, their return is around 85–100 percent. With the same money.

The third – worst scenario: started DCA near the top. After the drop their portfolio is down 40 percent. They continue buying every month. After 3–4 years they get back to zero. Psychologically catastrophic. After such an experience most people leave the market at the bottom and never come back.

Japan, 1989. The Nikkei 225 reached 38,915 points – everyone believed the twenty-first century belonged to Japan. Of the world’s 20 largest companies, 13 were Japanese. Tokyo real estate cost 350 times more than Manhattan. Those who invested were kings.

Then the Nikkei fell about 80 percent – to roughly 7,800 points in 2003. Recovery to the pre-crisis level took 34 years: in early 2024 the index finally reached its 1989 peak. Adjusted for inflation – still in the red. The person who started DCA a year before the peak spent more than twenty years watching their portfolio in the red. The worst cohorts – those who started investing in 1979–1983 – received a 2.61 percent annual return over 43 years. Inflation ate that return.

“But that’s Japan, it won’t happen to us.” Fine. Let’s look at America.

Dot-com bubble, 2000. S&P 500 fell 49 percent. It recovered to pre-crisis levels only in October 2007 – 7 years later. But then – the 2008 financial crisis, another minus 57 percent. A true recovery above 2000 levels came only in 2013. Thirteen years. And NASDAQ? A 78 percent crash and recovery only in 2015 – fifteen years. If you were a NASDAQ DCA investor from 1999 – fifteen years of portfolio underperformance.

The 2008 financial crisis separately: S&P 500 fell 57 percent, the largest crash since World War II. Recovery – in 2013, five and a half years. The person who started DCA in 2006 or 2007 – for the first year or two everything grew, everything was fine. Then more than half the portfolio disappeared. And 5.5 years of waiting for it to return.

1929 recovery took 25 years.

These are not theories. These are numbers: Nikkei waited 34 years, NASDAQ – 15, S&P through two wipeouts – 13, after 1929 – 25 years. And every time someone said: “The long horizon smooths everything out.” It did. But that horizon was sometimes a person’s entire most productive period of life.

Other “Strategies”

Diversification. “Don’t keep all your eggs in one basket.” Sounds smart. But when your egg is just one – €10,000 – do you really need to scatter that one egg across 25 different baskets? Each basket has a fee. The total fee across 25 baskets is more than the return. Diversification is protection against ignorance. It’s nearly meaningless if you know what you’re doing. Giving a sniper a shotgun and telling them to hit a target at 800 meters – that’s diversification. A guarantee of not hitting anything specific.

60/40 portfolio. Sixty percent equities, forty percent bonds. The “eternal” allocation every advisor recommends. In 2022 both equities and bonds fell simultaneously. The “protection” didn’t work. 60/40 was built for a different era – low interest rates, stable inflation, a single hegemon. That era is over.

Pension funds. The fund officially earns 10–12 percent, while real inflation – the kind you feel in daily life in food prices, utilities, insurance – easily reaches 15 percent and more. Even investing you lose. Your investments are chasing inflation and can’t keep up. And the fund takes its percent – everything is fine for them.

Warren Buffett. He never did DCA in his life. He bought stocks when they were cheap. He exited positions when they were expensive – not at the very top, but expensive. He sits on cash and waits for “blood in the streets.” Then re-enters with all resources. Berkshire Hathaway is currently sitting on the largest cash position in its history – around $370–380 billion, more than double the previous record. He is selling. He is waiting. And you transfer a hundred euros automatically every month.

George Soros. His philosophy: “When I see a bubble – I act. I pour money in to inflate that bubble even further.” And then exits before the crash. He doesn’t do DCA. He doesn’t recommend diversifying across 25 baskets. He understands where in the cycle he is and acts accordingly. His fund needing DCA and recommending diversification after 25 years would have meant no longer recommending diversification. He understood when the cycle turns, and waited until the next one.

Howard Marks. His entire methodology is built on cycles. He writes about it, speaks about it, manages based on it. Oaktree’s portfolio management is fundamentally cycle-aware. When valuations are high – reduce risk. When low – add. Marks doesn’t believe in DCA. He believes in understanding context, in which the next decade’s return is already embedded.

Ray Dalio. His “all-weather” strategy is actually not diversification for its own sake – it is a cycle-awareness tool. He doesn’t buy everything equally. He balances based on what each cycle phase favours. His manufacturing sector profitability indicators reflect the cycle. Those who track this cycle see turns earlier.

Not one of these people did DCA and not one recommended diversifying across 25 baskets. They understood where they were in the cycle and acted accordingly.

The Escalator Generation

The 2009–2023 bull market was unusual not so much for the pace of growth as for its structure. The Federal Reserve injected about ten trillion dollars into the system during that period – waves of cheap liquidity that lifted everything: equities, real estate, bonds, cryptocurrencies. DCA worked during that period not because the strategy was good – but because the central bank was systematically inflating the prices of all assets upward. When that wind changes – and today all central bank liquidity indicators show contraction – DCA stops being a strategy. It becomes an anchor.

The DCA generation born between 2009 and 2023 experienced only one direction – up. They were never tested. They don’t know what it’s like to watch a portfolio in the red for two, three, five years. They confuse the escalator with their own legs.

People who started investing before 2008 – they experienced depression, felt the pain, and most of them either left the market at the bottom having realized losses, or waited 13–15 years to return to zero.

I wish everyone under forty would understand: the escalator going up doesn’t rise forever. Wipeouts happen. And when they happen – DCA doesn’t become your friend. It becomes your enemy, because you’re buying every month at lower and lower prices, but your portfolio is still in the red. And psychologically that is more brutal than anything they told you about “the long horizon.”

A Direct Question

You’re a good person who invests every month on the fifteenth. You’ve had a nice result. But – when did you enter the market? When did you start this journey of yours? That is the essential moment on which everyone can get caught.

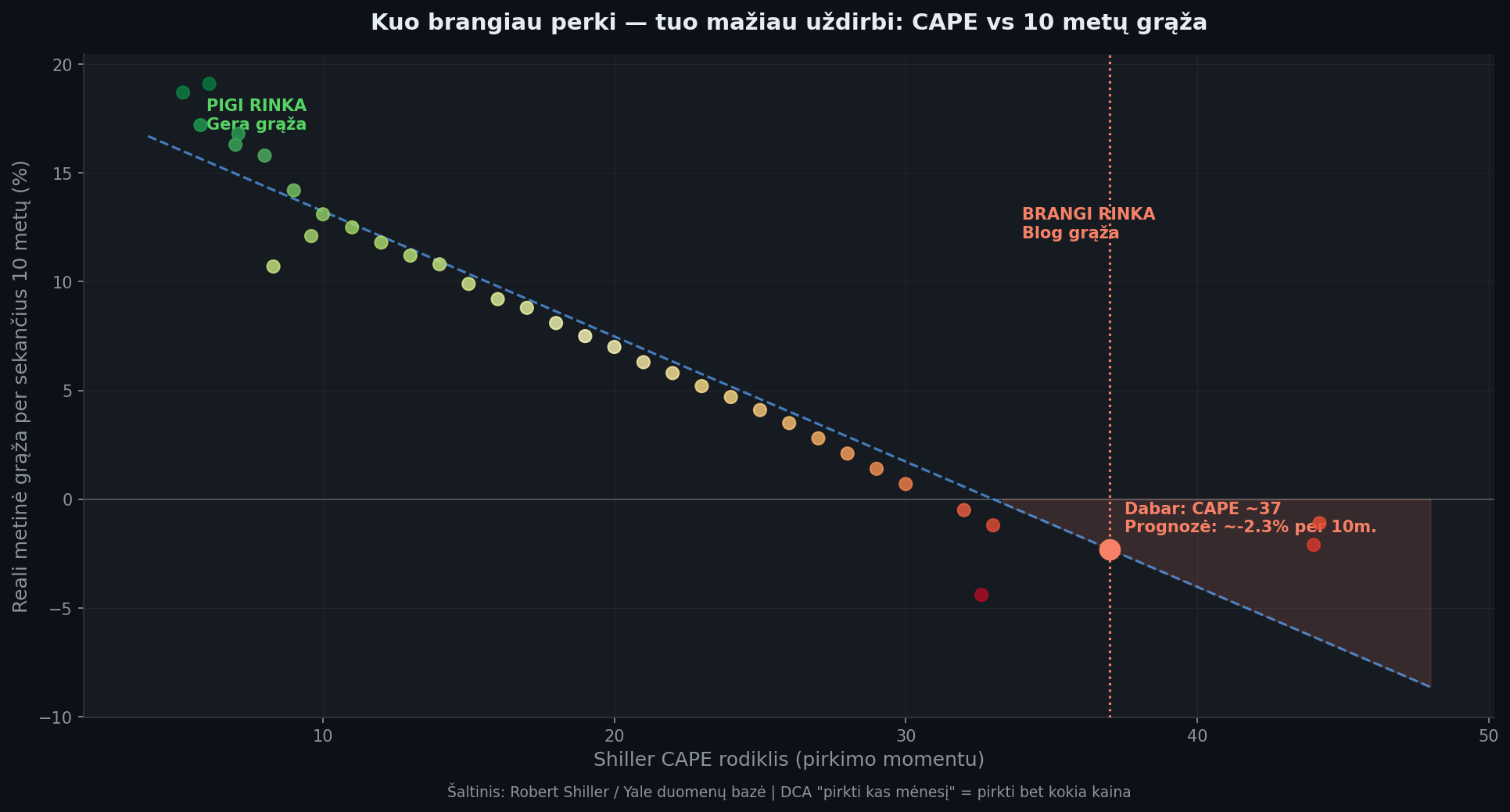

The CAPE ratio – the cyclically adjusted price-to-earnings ratio, which measures how expensive the market is relative to a ten-year earnings average – is currently around 37. That means you’re buying equities more expensively than usual, and this is the second highest level since 1871. The Buffett indicator – the ratio of total market capitalisation to GDP, showing whether the size of the stock market matches real economic strength – exceeded 220 percent at the start of 2026. That is the “Significantly Overvalued” zone. This is not an opinion – these are numbers.

If you start DCA now – are you mentally prepared to watch your portfolio in the red for the next six or seven years? Because if the cycles are right – that is exactly what will happen. I may be wrong. Cycles can last longer than logic allows. But the odds are not in your favour right now.

Should your strategy perhaps be different? Focus on what will still shoot upward. Take profits. Wait for the wipeout. And re-enter the market.

“Yeah, speculation, gambling” – say those who have never read a single book about cycles. But let’s look from the other side: if you had waited for the bottom in 2008, 2002, 1929 – and entered when everything was cheap – your long-term return would not be 7–8 percent annually. It would be 20–30 percent. With the same money. With less risk, because you bought cheap.

That is not speculation. That is cycle literacy. It is a skill that can be learned. It requires reading Howard Marks, understanding the Buffett indicator, watching the CAPE ratio, tracking the Fed’s liquidity cycle. It is not simple. But it is learnable.

I am not telling you to stop investing. I am telling you to stop letting the financial industry sell you a tactic as if it were a strategy.

If you are currently in the market – think about your exit. Not panic-selling, but conscious de-risking. Reduce exposure. Build a cash reserve. Prepare for the entry point that will come.

If you are not yet in the market – rethink your strategy.

Catching a falling knife at floor level is better than holding a knife gripped at the very top. And still pressing that knife in.

This is not financial advice. This is one person’s view, based on cycle analysis, historical data and personal experience. Always do your own research before making decisions.

If this letter helped you see something differently – share it with a friend who transfers a hundred euros automatically every month. And if you want to continue the conversation – reply directly to this email. I read everything.

Meška